Date for reporting open balance for ITC reversal extdd to 31.1.24. Facility to amend declared open balance to be available till 29.2.24

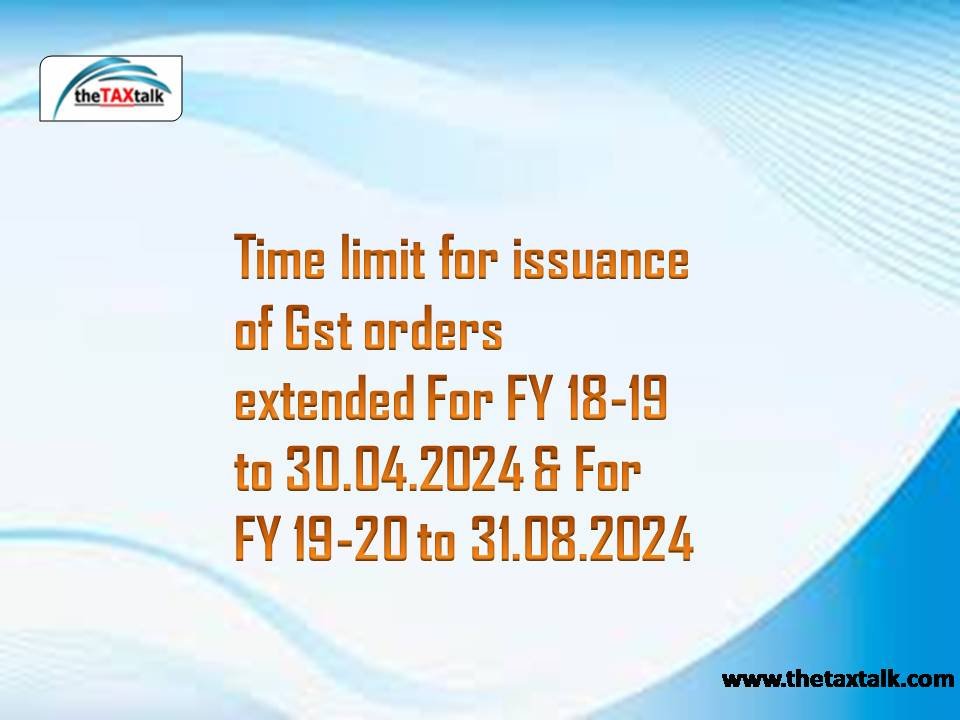

Time limit for issuance of Gst orders extended For FY 18-19 to 30.04.2024 & For FY 19-20 to 31.08.2024

Service of Notice through GST Portal to Assessee whose Registration was Cancelled is Invalid: Madras HC

Decision To Cancel GST Registration With Retrospective Effect Must Be Based On Some Objective Criteria: Delhi High Court

Whether salary received by a working partner from a partnership firm has to be included in Aggregate turnover for the purposes of GST

Short Overview of the amendments related to the Safe Harbour Rules for intra-group loans applicable from April 1, 2024.

No ITC Reversal of GST by customer unless Revenue cannot recover dues from supplier post proceedings against him.