Order under section 119 of the income-tax Act, 1961 (the Act) providing exclusions to section 144B of the Act.

The “project completion method” is one of the recognized methods of accounting and cannot be rejected by the AO

No addition under Section 50C for a difference of up to 10% of stamp duty value on a retrospective basis

Interest income by Developer firm is assessable as Business Income & not as Income from Other Source Income: Adv. Ravindra Poojary

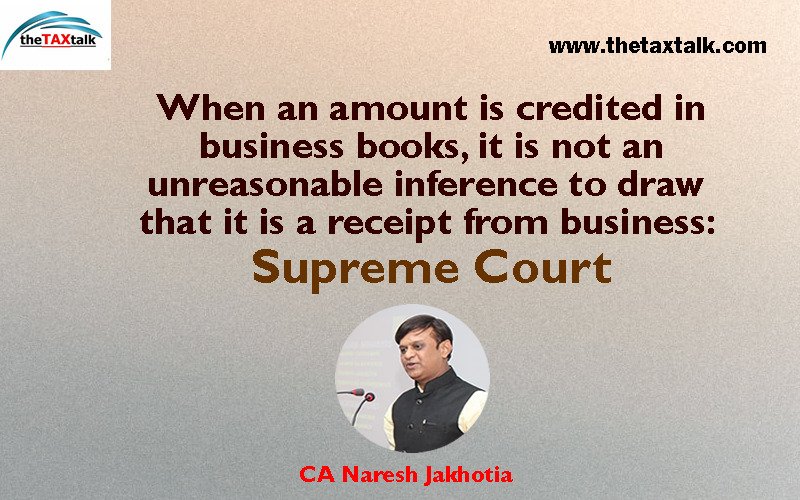

When an amount is credited in business books, it is not an unreasonable inference to draw that it is a receipt from business: Supreme Court

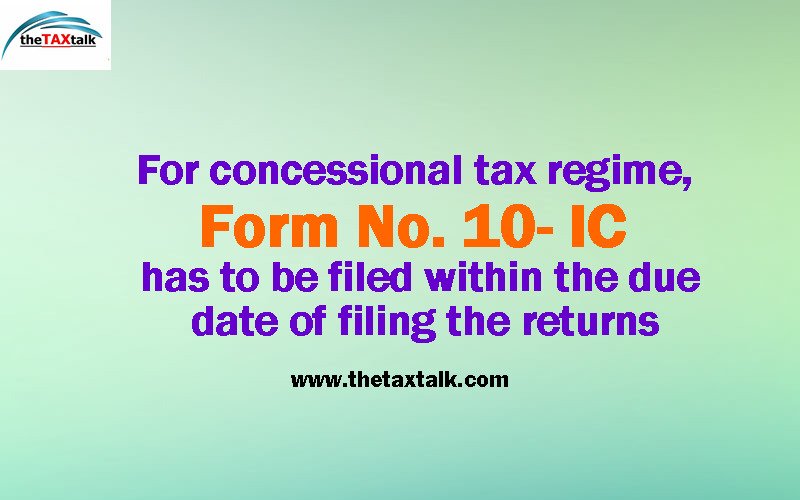

For concessional tax regime, Form No. 10- IC has to be filed within the due date of filing the returns

Improper & Hurried Order by the Officers: Tax Bar Association, Indore made an Honest Representation seeking an extension of the date of completing the Assessment

TDS done on Gross amount received from Life Insurance Companies- Whether entire amount is taxable or only the income therin is taxable?

Whether a witness can be summoned to appear outside his city of residence in case of an offence under Prohibition of Money Laundering Act (PMLA)?

Validity of Income Tax Notice not available at the income tax portal at the time of issuance but uploaded afterwards