significant observations and recommendations emanating out of the Performance Audit conducted on ‘Functioning of Unique Identification Authority of India’ by CAG

Whether Tax exemption promised can be withdrawn by subsequent notification under the Kerala State Sales Tax Act?

Technical breach without any intention to evade tax: High court ordered to release the vehicle and the consignment to the petitioner

Taxpayer can exercise option of Writ petition even if alternative remedy in the form of CIT (A) is available

Same issue examined by ITAT in earlier years, whether disallowance for subsequent years can be done by the AO?

Re-assessment notice issued without prior approval of jurisdictional CIT contravenes mandate of Section 151(2) and hence invalid: Banglore ITAT

Time spent in appeal filed with bona fide mistake to be excluded for computing limitation period for sec. 264 revision: HC

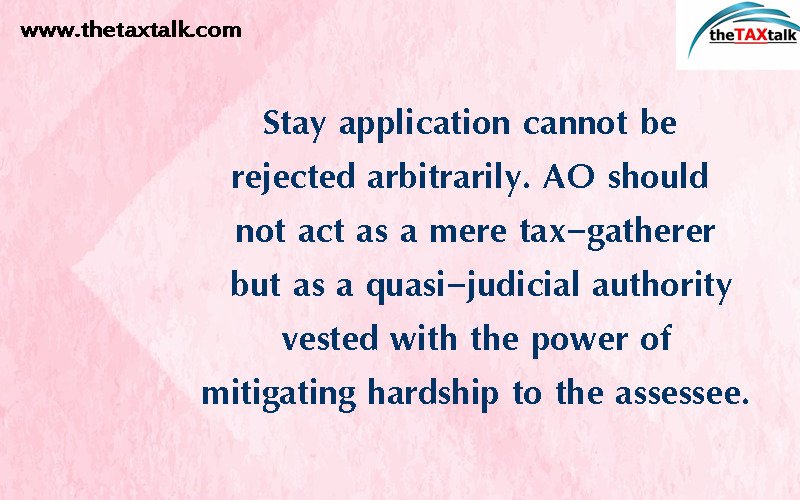

Stay application cannot be rejected arbitrarily. AO should not act as a mere tax-gatherer but as a quasi-judicial authority vested with the power of mitigating hardship to the assessee.