Can a taxpayer claim exemption under both Section 54 and Section 54F by investing in a single new house?

Once, the issue has been decided by the Hon’ble High Court in favour of the assessee, on the same very issue assessment for the subsequent assessment years cannot be reopened

Reopening order quashed as it was on the erroneous assumption that no return of income was filed – whereas the return was duly on record.

ITAT quashed the entire re-assessment proceedings holding it to be barred by limitation as the escaped income was less than 50 Lakhs and the reassessment was initiated after the expiry of 3 years.

DTAA Rate vs. Section 206AA: Where a beneficial treaty rate exists, that rate must apply-even if the non-resident does not have a PAN

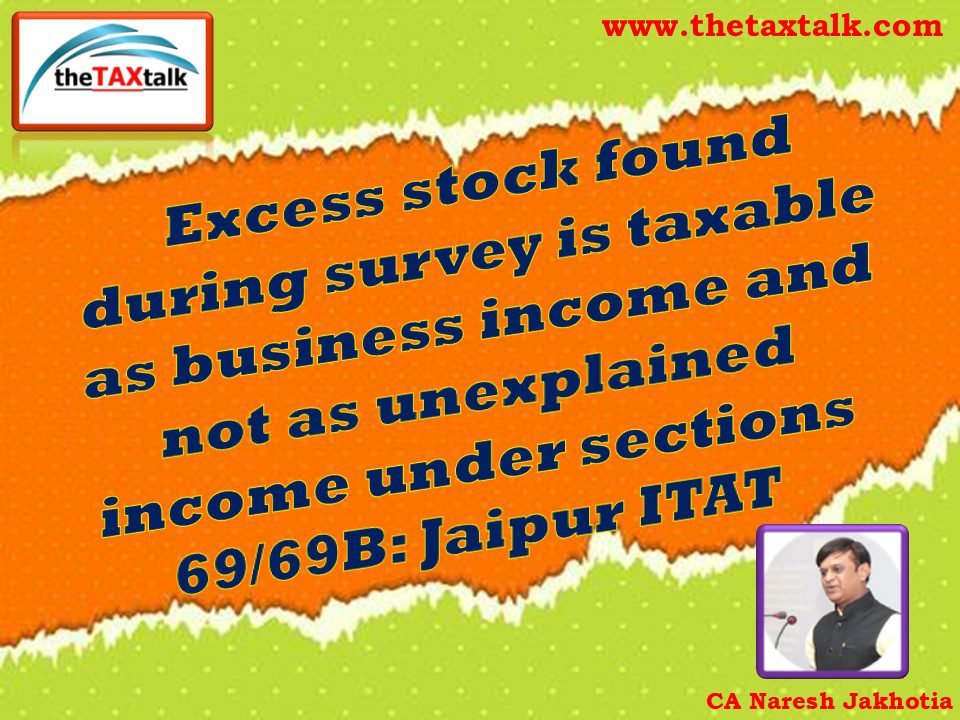

Excess stock found during survey is taxable as business income and not as unexplained income under sections 69/69B: Jaipur ITAT

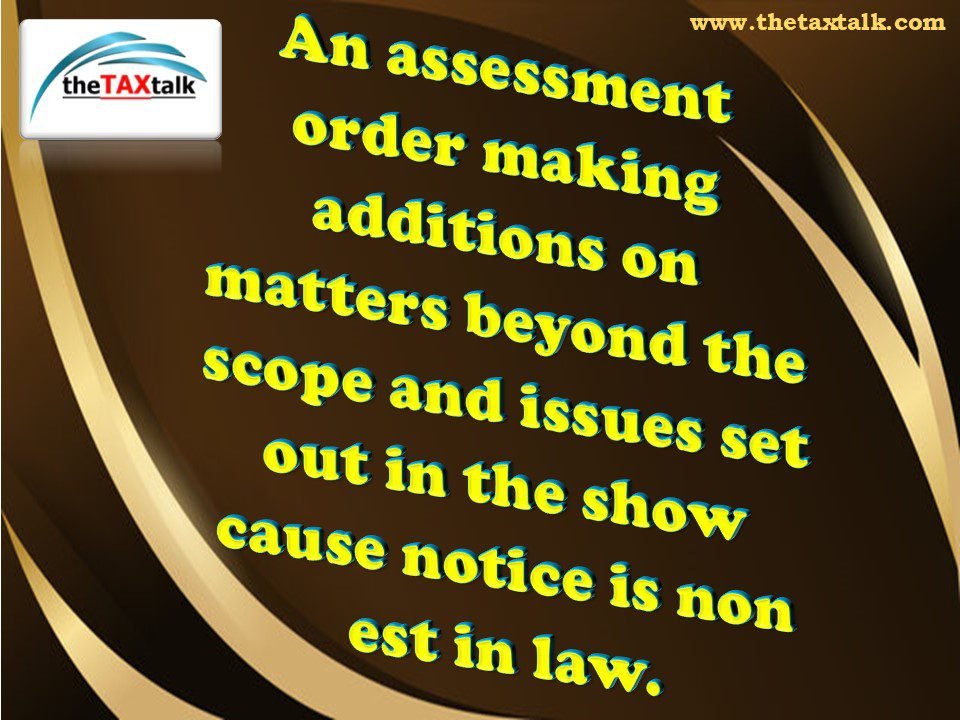

An assessment order making additions on matters beyond the scope and issues set out in the show cause notice is non est in law.

When the original reason fails, the AO cannot make any other addition in a reassessment proceeding: ITAT

Addition done during assessment is invalid if it is done without waiting for the DVO Report: ITAT Ahmedabad

Purchase from Government – No addition under Section 56(2)(x) for purchase below stamp duty valuation: ITAT