Books Rejected, Sales Recorded, Section 68 Invoked? ITAT Mumbai Draws a Clear Line in Demonetisation Cash Deposit Cases

Mumbai ITAT Strikes Down Section 68 Additions Based Solely on Entry Operator Statement: A Strong Reaffirmation of Law and Natural Justice

ROC Vijayawada penalized auditor for failing to qualify or comments or give opinion in the audit report

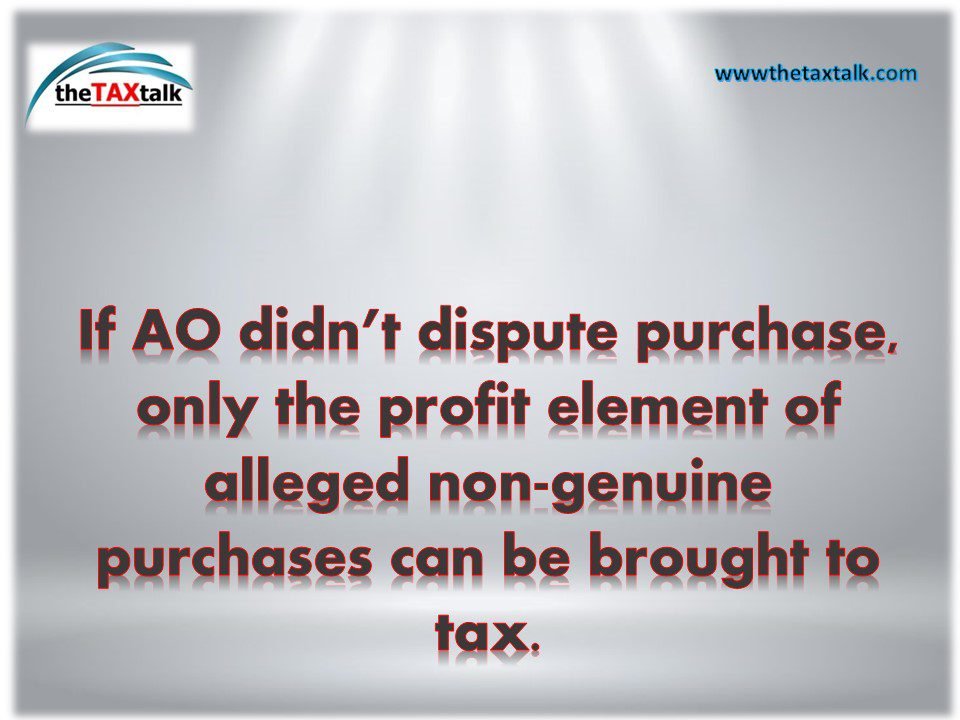

If AO didn’t dispute purchase, only the profit element of alleged non-genuine purchases can be brought to tax.

Allahabad High Court Protects Genuine Input Tax Credit: ITC Cannot Be Denied Merely Due to Subsequent Cancellation of Supplier’s GST Registration

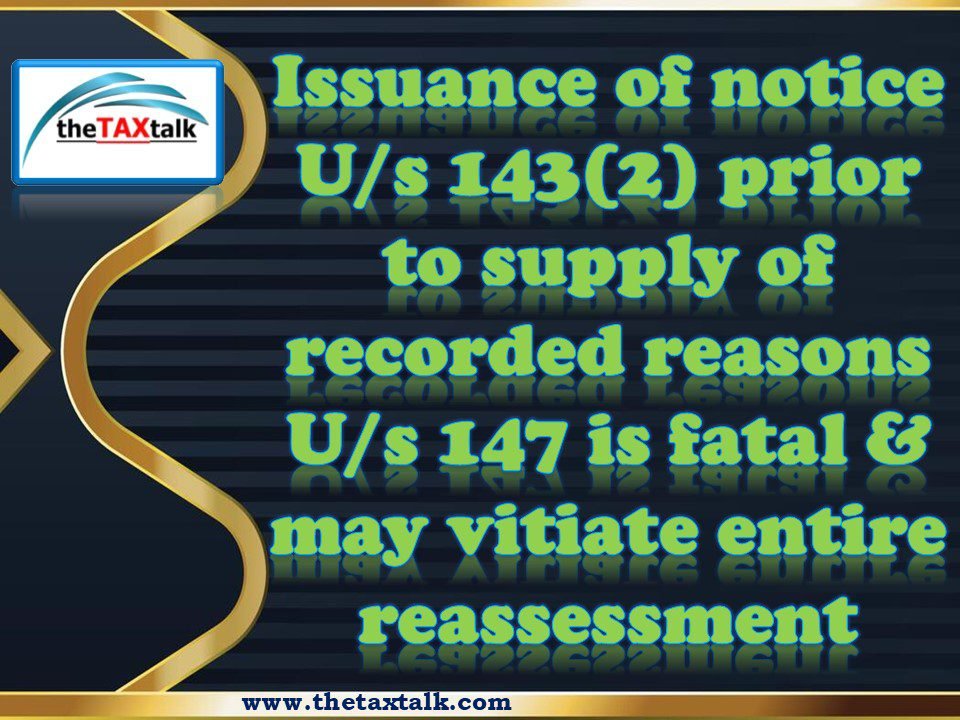

Issuance of notice U/s 143(2) prior to supply of recorded reasons U/s 147 is fatal & may vitiate entire reassessment