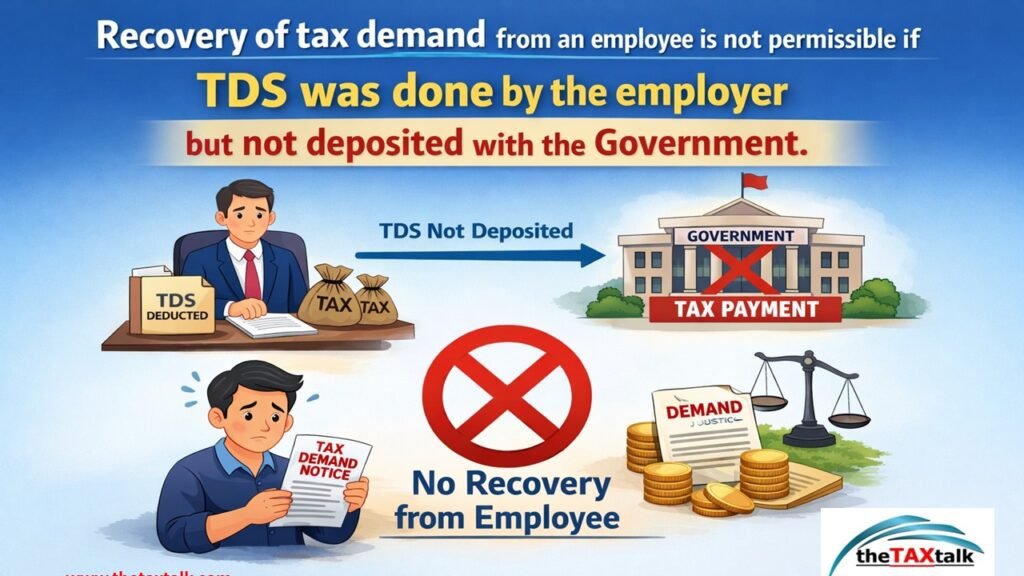

Recovery of tax demand from an employee is not permissible if TDS was done by the employer but not deposited with the Government.

Vivad Se Vishwas Not Concluded? Appeal Must Be Heard on Merits — ITAT Mumbai Deletes Demonetisation Cash Addition