Income Tax Search and Seizure: Importance of Statement u/s 132(4) of the Income Tax Act’1961, Retraction thereof.

No deemed dividend if assessee didn’t get benefit from loans advanced to Co. in which he was substantially interested

No Prosecution could be launched unless it is proved that unaccounted transactions were liable for payment of tax

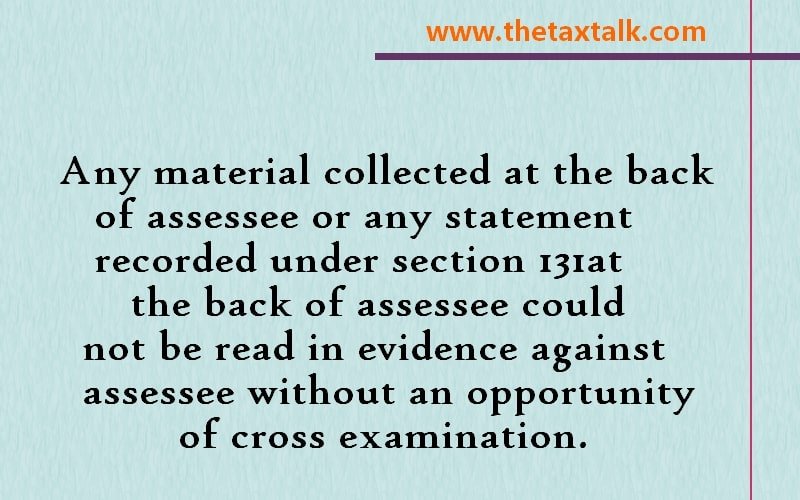

Any material collected at the back of assessee or any statement recorded under section 131 at the back of assessee could not be read in evidence against assessee without an opportunity of cross examination.

CBI Arrests Three Officials of Customs Department in a Bribery Case of Rs. Four Lakh, and Recovers Cash of Rs. 20 Lakh (Approx) During Searches

Amazing Judgment : Gain received on personal loan due to forex fluctuation is capital receipt not liable to tax: ITAT

Appeal to Finance Minister for Reschedulement of Loan, waiver or deferment of interest & various other measures by Respected Shri Suresh Prabhu