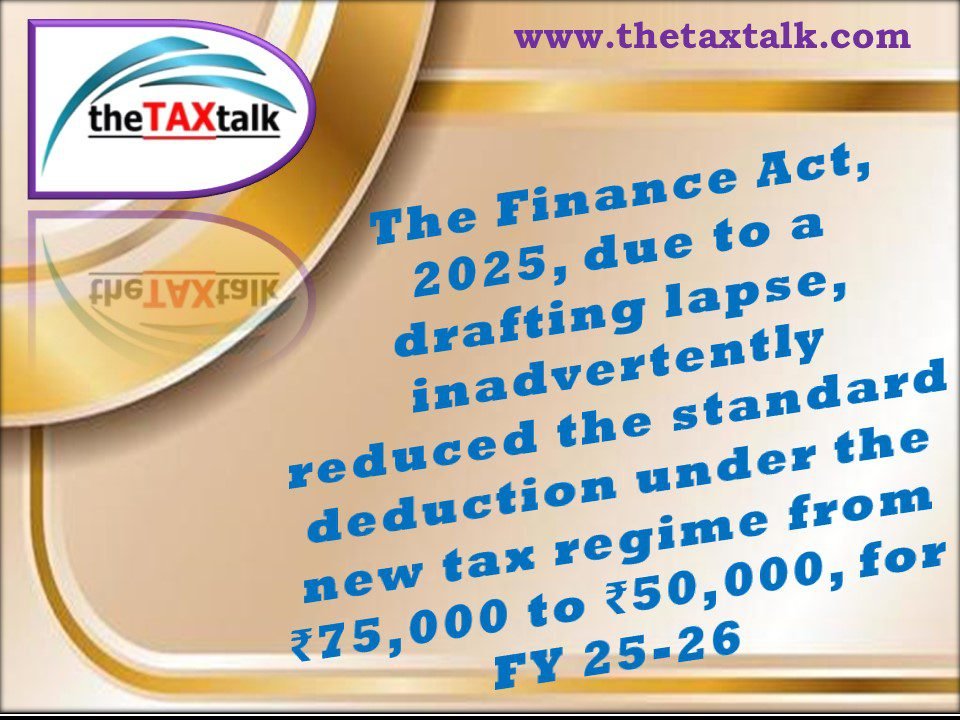

The Finance Act, 2025, due to a drafting lapse, inadvertently reduced the standard deduction under the new tax regime from ₹75,000 to ₹50,000, for FY 25-26

Additional Ground Can Be Raised at Hearing-Even If Not Taken Before Lower Authorities or in Cross-Objection!

Denial of exemption under Section 11 made by CPC under Section 143(1) – ITAT Mumbai grant relief to Trust

Seizure of Goods in Transit Without Notice Under Section 129(3): Andhra Pradesh High Court’s Landmark Ruling

Vintage car sale is subject to capital gains tax if there’s no proof of its personal use: Bombay High Court

Widow entitled to TDS in the name of her late husband, after she had declared his income in her own tax returns (ITRs): ITAT

Representation for General Amnesty Scheme under earlier law as well as Current Profession Tax, MVAT & CST Acts for the period up to 31/03/2025 – By BJP Professional Cell

Urgent Representation for Extending date for filing return in form GSTR 3B for the month July 2025 – By BJP Professional Cell