Medical Store run by Charitable Trust would require GST Registration, and that Medical Store providing medicines even if supplied at lower rate would amount to supply of goods.

Capital gain exemption could not be denied to the assessee for the reason that the sale deed has not been executed by the builder

Income Tax Search and Seizure: Controversy in computing the period of limitation to frame search assessments

Relaxation on levy of additional fees in filing of e-forms AOC-4, AOC-4 (CFS), AOC-4 XBRL, AOC-4 Non-XBRL and MGT-7/MGT-7A

Income Tax Raids on two prominent groups of Raipur and Korba: Unaccounted transactions of more than Rs. 200 crore found

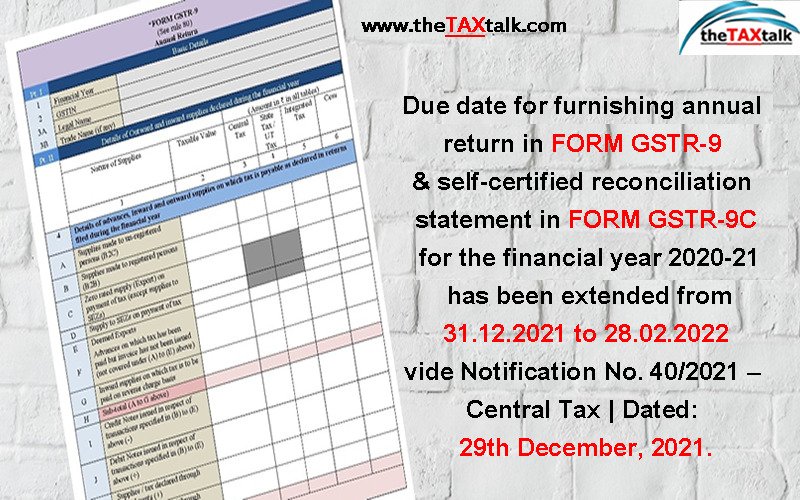

Due date for furnishing annual return in FORM GSTR-9 & self-certified reconciliation statement in FORM GSTR-9C for the financial year 2020-21 has been extended from 31.12.2021 to 28.02.2022 vide Notification No. 40/2021 – Central Tax | Dated: 29th December, 2021.

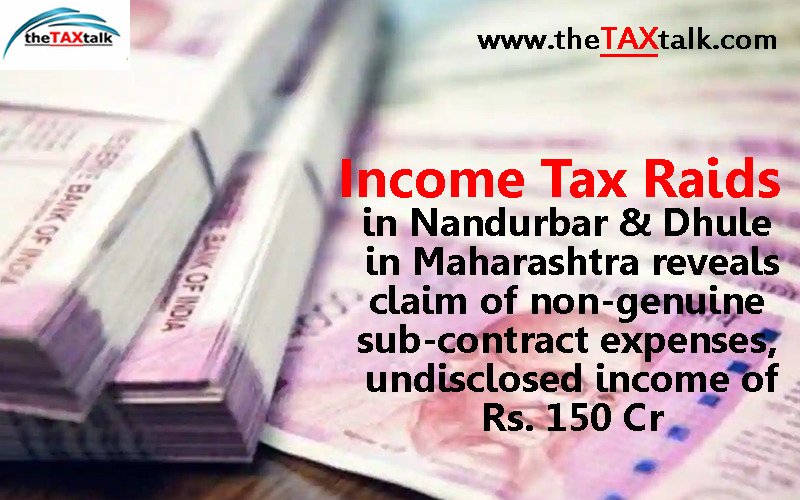

Income Tax Raids in Nandurbar & Dhule in Maharasthra reveals claim of non-genuine sub-contract expenses, undisclosed income of Rs. 150 Cr

Re-opening of assessment is valid if cash payments over Rs. 20,000/- made by assessee escape scrutiny u/s 40A