![]()

Whether due date for audit is extended for charitable trust also or not?

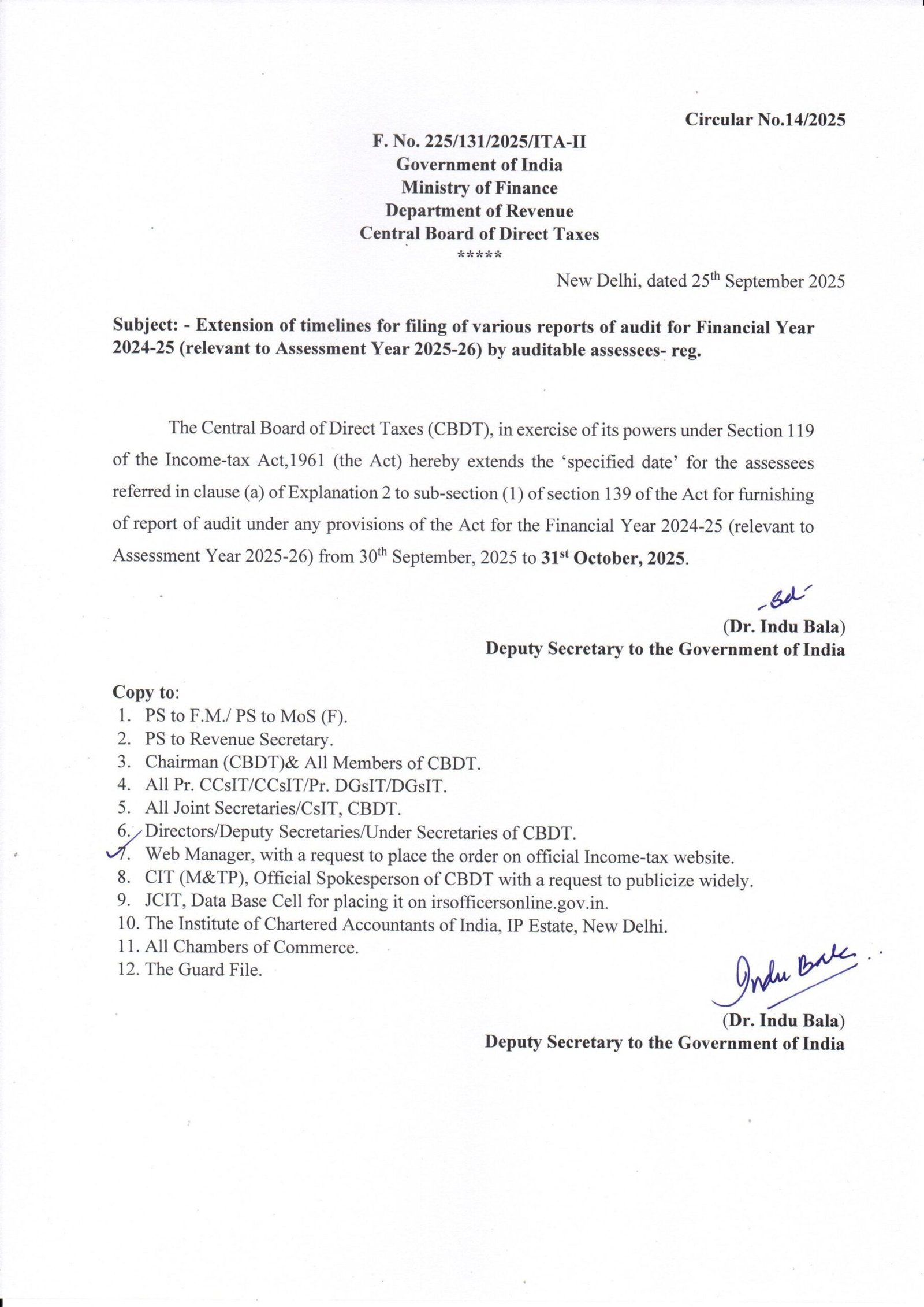

CBDT has recently extended the due date of filing the audit report. The circular reads as under:

The question which is raised is whether the extension is only for business class assessee & companies or even for charitable trust?

It may be noted that what is extended is

a. Assessee covered by section 139(1)- Explanation 2 – Clause (1)

b. Extension is of Specified date

The said explanation to clause (a) to explanation to section 139 (1) reads as under:

Explanation 2.-In this sub-section, “due date” means,-

(a) where the assessee other than an assessee referred to in clause (aa) is-

(i) a company; or

(ii) a person (other than a company) whose accounts are required to be audited under this Act or under any other law for the time being in force; or

(iii) a partner of a firm whose accounts are required to be audited under this Act or under any other law for the time being in force or the spouse of such partner if the provisions of section 5A applies to such spouse, the 31st day of October of the assessment year;

In short, trust is covered by extension as the extension is provided for ‘a person (other than a company) whose accounts are required to be audited under this Act or under any other law for the time being in force.’

Now, come to specified date. The specified date is mentioned in section 44AB as well as in section 12A(1)(b) which provides for audit of charitable trust. Let s analyse section 12AB.

Section 12A(1)(b) reads as under:

Conditions for applicability of sections 11 and 12.

12A. (1) The provisions of section 11 and section 12 shall not apply in relation to the income of any trust or institution unless the following conditions are fulfilled, namely:-

(a) ——————–

——————-

(b) where the total income of the trust or institution as computed under this Act without giving effect to the provisions of sections 11 and 12 exceeds the maximum amount which is not chargeable to income-tax in any previous year,-

(i) the books of account and other documents have been kept and maintained in such form and manner and at such place, as may be prescribed; and

(ii) the accounts of the trust or institution for that year have been audited by an accountant defined in the Explanation below sub-section (2) of section 288 before the specified date referred to in section 44AB and the person in receipt of the income furnishes by that date the report of such audit in the prescribed form duly signed and verified by such accountant and setting forth such particulars, as may be prescribed;

In short, the specified date in section 12A also referred to section 44AB only. This reference is only for specified date and nothing more than that.

Here is the breakdown of the relevant provision:

• Section 12A of the Income-tax Act, 1961, deals with the conditions for the applicability of Sections 11 and 12 (which provide the exemption for income of charitable or religious trusts).

• Section 12A(1)(b) states the condition related to the audit report:

• Where the total income of the trust (computed without giving effect to the provisions of Section 11 and 12) exceeds the maximum amount not chargeable to tax, the accounts must be audited by a Chartered Accountant.

• It requires that the audit report in the prescribed form (Form 10B or Form 10BB, as applicable) must be furnished by the specified date.

• The term “specified date” is defined in the context of charitable trusts (Section 12A) and other assessees (Section 44AB) as one month prior to the due date for furnishing the return of income under sub-section (1) of Section 139.

Consequence of Late Filing:

If the audit report (Form 10B/10BB) is not furnished by the specified date (one month before the ITR due date), the trust or institution will generally lose the benefit of the exemption under Sections 11 and 12 of the Income-tax Act for that assessment year. Consequently, its income will be taxed at the normal rates.

Since the specified date is extended, it is extended for section 44AB as well as section 12A(1)(b). It may be noted that the extension circular by CBDT only mentions specified date is extended without referring anything about section 44AB and section 12A.

In short, wherever specified date for audit is there, all stand extended to 31st October.

{kind=link}

{kind=link}