![]()

Rule 11UA amended by CBDT for angel tax on funds raised from non-residants.

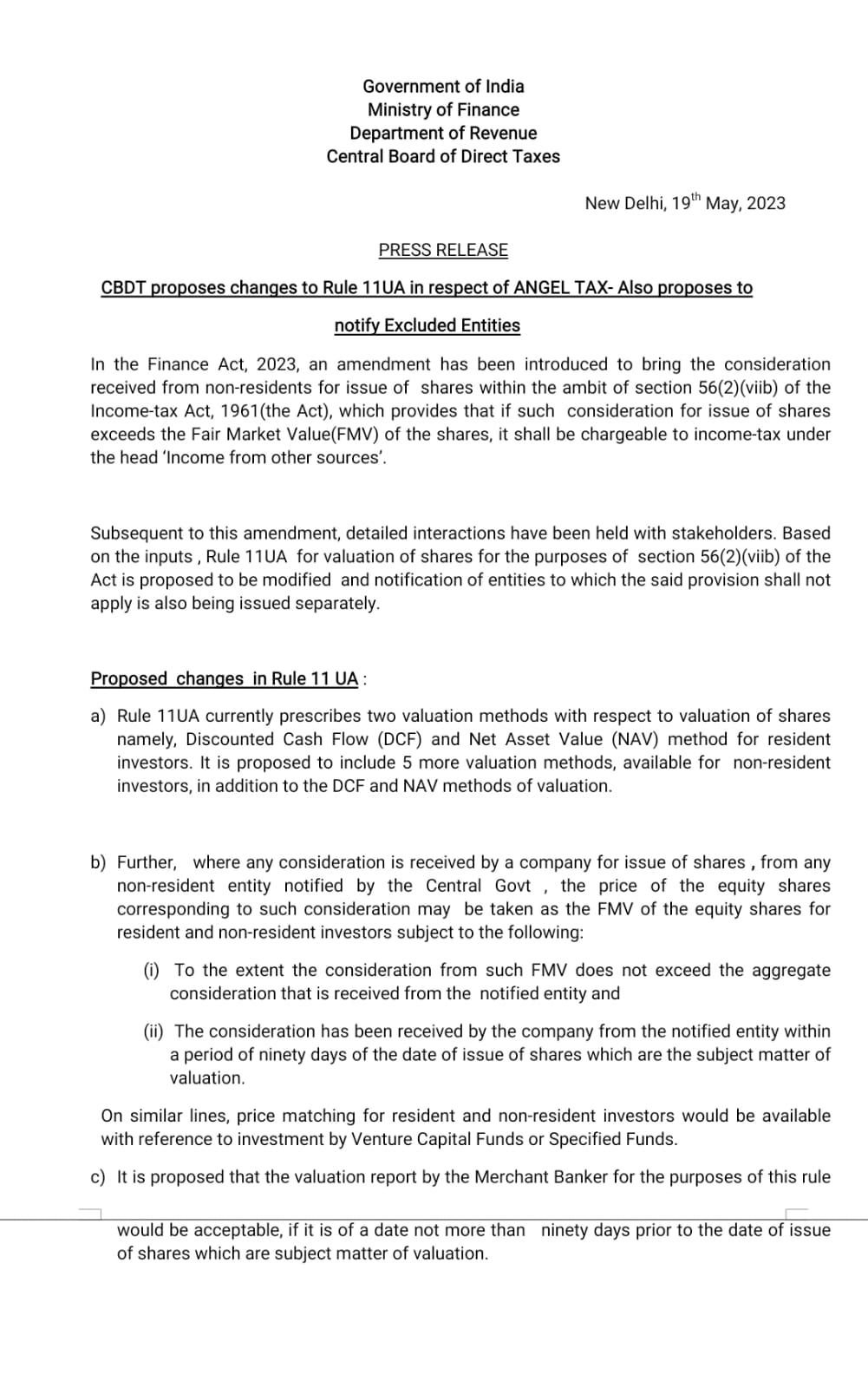

The CBDT has issued Press Release proposing changes to Rule 11UA for angel tax on funds raised from non-residents. Among the major changes being considered, the notable ones include:

1. Deeming the price per share of equity shares for consideration raised from notified non-resident entities as the FMV per equity share for both residents and non-residents, subject to safeguards

2. Prescribing five additional methods of valuation (in addition to the existing DCF and NAV) to provide for different valuation approaches for new-age businesses

3. Prescribing a list of excluded entities which shall be exempted – amongst others, these include FPIs, sovereign wealth funds, pension funds and all pooling vehicles with more than 50 investors

4. Exempting specified DPIIT recognised start-ups from the applicability of the provisions.

The draft rules will be put out for public comments before being notified.

It will be interesting to watch out for the draft rules, including the new valuation methodologies. Deeming value at which funds are raised from certain prescribed non-residents as the FMV is an interesting proposition as it also aligns with the FEMA provisions which permit raising funds from non-residents at a value higher than the certified FMV as per internationally acceptable valuation methodologies.

The copy of here CBDT press release is as under :

{kind=link}

{kind=link}