![]()

Interplay of Sec 44AA, 44AB and 44AD of the Income Tax Act,1961 By CA. R.S.Kalra

Author

CA. R.S.Kalra

ca.rskalra@yahoo.com

Section 44AB of the income-tax Act, 1961, which provides for tax audit of certain taxpayers, has been amended in the recent past in order to relax the compliance burden on small taxpayers. However, while these amendments are well-intentioned, they have increased confusion amongst taxpayers. We know that there are various monetary limits u/s Sec 44AA , 44AB and Sec 44AD of the Act relating to maintenance of books of accounts and audit. These provisions have created ambiguity among taxpayers and professionals. There is lack of clarity amongst the stakeholders of business community regarding the conduct of audit in relation to the provisions of sec 44AB(a) and sec 44AB(e) of the Act. It is worth mentioning here that tax audit u/s 44AB is applicable when the turnover of the assessee is exceeding Rs.1 crore and the assessee has a lot of questions in his mind regarding the limit of turnover for audit or for maintenance of books of accounts.

Now let us start our journey to understand the provisions of these sections and their interplay with sec 44AD of the Act.

Firstly we have to read the relevant provisions of sec 44AB which are as under:

44AB. 6Every person,—

(a) carrying on business shall, if his total sales, turnover or gross receipts, as the case may be, in business exceed or exceeds one crore rupees in any previous year 7[***]:

8[Provided that in the case of a person whose—

(a) aggregate of all amounts received including amount received for sales, turnover or gross receipts during the previous year, in cash, does not exceed five per cent of the said amount; and

(b) aggregate of all payments made including amount incurred for expenditure, in cash, during the previous year does not exceed five per cent of the said payment:

9[Provided further that for the purposes of this clause, the payment or receipt, as the case may be, by a cheque drawn on a bank or by a bank draft, which is not account payee, shall be deemed to be the payment or receipt, as the case may be, in cash,]

this clause shall have effect as if for the words “one crore rupees”, the words “10[ten] crore rupees” had been substituted; or]

(b) carrying on profession shall, if his gross receipts in profession exceed fifty lacs rupees in any previous year; or

(c) carrying on the business shall, if the profits and gains from the business are deemed to be the profits and gains of such person under section 44AE or section 44BB or section 44BBB, as the case may be, and he has claimed his income to be lower than the profits or gains so deemed to be the profits and gains of his business, as the case may be, in any previous year; or

(d) carrying on the profession shall, if the profits and gains from the profession are deemed to be the profits and gains of such person under section 44ADA and he has claimed such income to be lower than the profits and gains so deemed to be the profits and gains of his profession and his income exceeds the maximum amount which is not chargeable to income-tax in any previous year; or

(e) carrying on the business shall, if the provisions of sub-section (4) of section 44AD are applicable in his case and his income exceeds the maximum amount which is not chargeable to income-tax in any previous year,

get his accounts of such previous year audited by an accountant before the specified date and furnish by that date the report of such audit in the prescribed form duly signed and verified by such accountant and setting forth such particulars as may be prescribed :

Provided that this section shall not apply to the person, who declares profits and gains for the previous year in accordance with the provisions of sub-section (1) of section 44AD and his total sales, turnover or gross receipts, as the case may be, in business does not exceed two crore rupees in such previous year:

Sec 44AB(a) – Every person carrying on business shall maintain books of accounts and get them audited from a Chartered Accountant if total sales, turnover or gross receipt from business during the previous year exceeds Rs.1 crore.

44AB(e) Every person carrying on the business shall, if the provisions of sub-section (4) of section 44AD are applicable in his case and his income exceeds the maximum amount which is not chargeable to income-tax in any previous year

Analysis of the provisions of Sec 44AB(a) of the Act

Every person –

(a) carrying on business shall,

-

if his total sales, turnover or gross receipts,

-

as the case may be,

-

in business exceed or exceeds

-

one crore rupees in any previous year

Following proviso is inserted after clause (a) of section 44AB by the Finance Act, 2021, w.e.f. 1-4-2021:

[Provided that in the case of a person whose—

-

aggregate of all amounts received including amount received for sales, turnover or gross receipts during the previous year,

in cash,

does not exceed five per cent of the said amount; and

(b) aggregate of all payments made including amount incurred for expenditure,

in cash,

During the previous year does not exceed five per cent of the said payment,

this clause shall have effect as if for the words “one crore rupees”,

the words “ten crore rupees” had been substituted; or

Analysis of the provisions of Sec 44AB(e) of the Act

It is to be noted that u/s 44AB(e) of the Act, an assessee is required to get his books of account audited who is carrying on the business and is not eligible to claim presumptive taxation under Section 44AD for 5 subsequent years due to opting for presumptive taxation in one tax year and not opting for presumptive tax for any of the subsequent 5 consecutive years provided his income exceeds maximum amount not chargeable to tax. In other words we can say that for the applicability of Sec 44AB(e) of the Act, the assessee must fulfill following two conditions : |

(a) The assessee is not eligible for presumptive taxation u/s 44AD for subsequent 5 years, due to opting of presumptive taxation u/s 44AD in any previous year and not opting sec 44AD in any of subsequent 5 consecutive Assessment years.

(b) His income exceeds the basic exemption limit.

44AA. (2) Every person carrying on business or profession [not being a profession referred to in sub-section (1)] shall,—

(i) if his income from business or profession exceeds one lacs twenty thousand rupees or his total sales, turnover or gross receipts, as the case may be, in business or profession exceed or exceeds ten lacs rupees in any one of the three years immediately preceding the previous year; or

(ii) where the business or profession is newly set up in any previous year, if his income from business or profession is likely to exceed one lacs twenty thousand rupees or his total sales, turnover or gross receipts, as the case may be, in business or profession are or is likely to exceed ten lacs rupees, during such previous year; or

(iii) where the profits and gains from the business are deemed to be the profits and gains of the assessee under section 44AE or section 44BB or section 44BBB, as the case may be, and the assessee has claimed his income to be lower than the profits or gains so deemed to be the profits and gains of his business, as the case may be, during such previous year; or

(iv) where the provisions of sub-section (4) of section 44AD are applicable in his case and his income exceeds the maximum amount which is not chargeable to income-tax in any previous year,

keep and maintain such books of account and other documents as may enable the Assessing Officer to compute his total income in accordance with the provisions of this Act:

Provided that in the case of a person being an individual or a Hindu undivided family, the provisions of clause (i) and clause (ii) shall have effect, as if for the words “one lacs twenty thousand rupees”, the words “two lacs fifty thousand rupees” had been substituted :

Provided further that in the case of a person being an individual or a Hindu undivided family, the provisions of clause (i) and clause (ii) shall have effect, as if for the words “ten lacs rupees”, the words “twenty-five lacs rupees” had been substituted.

Analysis Of the provisions of Sec 44AA(2) Of The Act

Sec 44AA(2) requires persons carrying on business to maintain books of accounts in certain cases. If a person is carrying on business, he is required to maintain books if his turnover exceeds Rs.10,00,000 or his profits from business exceeds Rs.1,20,000 in any of the three preceding years. Either of the condition satisfied will require person to maintain books because the word ‘or’ is used between the conditions. If any condition is satisfied in one or more years out of the three years preceding the previous year shall be required to maintain the books.

In case a new business is started during the previous year, if the turnover is likely to exceed Rs. 10,00,000 or profit is likely to exceed Rs.1,20,000 in such previous year, assessee is required to maintain books of accounts for that previous year. It is to be noted that the limit of Rs.1,20,000/- for Total Income & Rs.10,00,000/- for total sale receipts enhanced to Rs.2,50,000/- & Rs.25,00,000/- respectively in respect of Individuals/ HUF.

In respect of sec 44AA(2)(iv) of the Act, w.e.f. AY 2017-18, the assessee shall keep/maintain such books of account & other documents, if the provisions of Sec. 44AD(4) are applicable It means that if an assessee has declared profits as per sec 44AD(1) in any previous year and in the next 5 years he has failed to opt sec 44AD, then the assessee is not allowed to opt sec 44AD in the subsequent 5 years after the year in which he failed to opt sec 44AD. The assessee will be required to maintain books if sec 44AD(4) is applicable and his income exceeds the basic exemption limit.

From the reading od sec 44AA(2)(iv) of the Act, we draw following two conditions:

a.The assessee is not eligible for presumptive taxation u/s 44AD for subsequent 5 years, due to opting of presumptive taxation u/s 44AD in any previous year and not opting sec 44AD in any of subsequent 5 consecutive Assessment years.

b.His income exceeds the basic exemption limit

These provisions can be summarised with the help of the following table.

Category of Taxpayer |

Threshold Limits for Income |

Threshold Limits for Gross Turnover or Receipts |

|

Business |

Individual or HUF |

Rs.2,50,000 |

Rs.25 lacss in any of the 3 years immediately preceding the previous year |

Business |

Others |

Rs.1,20,000 |

Rs.10 lacss in any of the 3 years immediately preceding the previous year |

Presumptive Tax Scheme under Sec. 44AD |

Resident Individual or HUF |

Rs.2,50,000 |

Taxpayer opted for scheme in any of last 5 previous years but does not opt for in current year. |

Presumptive Tax Scheme under Sec. 44AD |

Resident Partnership Firm |

– |

Taxpayer opted for scheme in any of last 5 previous years but does not opt for in current year. |

Sec 44AD(4)

44AAD(4) Where an eligible assessee declares profit for any previous year in accordance with the provisions of this section and he declares profit for any of the five assessment years relevant to the previous year succeeding such previous year not in accordance with the provisions of sub-section (1), he shall not be eligible to claim the benefit of the provisions of this section for five assessment years subsequent to the assessment year relevant to the previous year in which the profit has not been declared in accordance with the provisions of sub-section (1).

Analysis of the provisions of Sec 44AD(4) of the Act

The above provision postulates as the following:

-

The assessee should have declared profit as per section 44AD for any previous year; and

-

The assessee should have declared profit not in accordance with section 44AD in any of the five assessment years succeeding the previous year in which profit was declared as per section 44AD as per condition (a).

44AD(5)Notwithstanding anything contained in the foregoing provisions of this section, an eligible assessee to whom the provisions of sub-section (4) are applicable and whose total income exceeds the maximum amount which is not chargeable to income-tax, shall be required to keep and maintain such books of account and other documents as required under sub-section (2) of section 44AA and get them audited and furnish a report of such audit as required under section 44AB.

Analysis of the provisions of Sec 44AD(5) of the Act

Sub Section 5 will be applicable if following conditions are satisfied.

-

An eligible assessee to whom the provisions of sub-section (4) are applicable; and

-

The total income of that assessee has exceeded the maximum amount which is not chargeable to income-tax.

In other words, sub-sections (4) and (5) are mutually inclusive. Provisions of sub-section (4) shall not be applicable to an assessee who never opted for the scheme in any of the earlier previous years, as it provides that the eligible assessee should have declared profits as per section 44AD for any previous year. Under this situation, assessees who have never ever opted for the scheme till the AY 2016-17 can enjoy the benefits by showing lesser profits for the subsequent assessment years.

On combined analysis of 44AA(2)(iv), 44AB(e) and 44AD(4) we can interpret that u/s 44AB(e) those assessees are required to get their books audited whose

-

Total income exceeds basic exemption limit.

-

Earlier assessee has declared income u/s 44AD in any previous year.

-

Even being eligible, assessee do not declare income as per sec 44AD in any of next 5 A.Ys in which he first declared income as per sec 44AD of the Act.

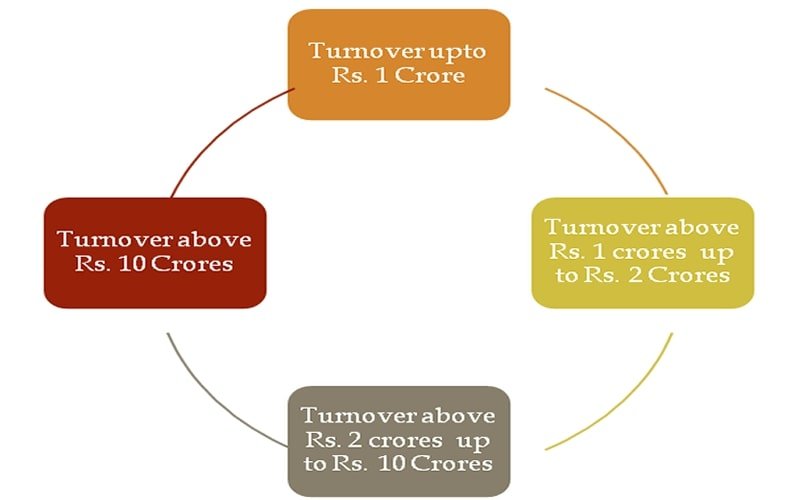

We can divide our study in the following 4 parts:

-

When business turnover is upto Rs.1 crore

-

When business turnover is exceeding Rs.1 crore but upto Rs.2 crore

-

When business turnover exceeding Rs.2 crore but upto Rs.10 crore

-

When business turnover exceeding Rs.10 crore

These all four categories can be shown as under

A. When business turnover is upto Rs.1 crore

If a person is having turnover/ gross receipts up to Rs.1 crore, clause (a) of Sec 44AB will not be applicable. If the person is declaring profits as per sec 44AD(1), he will not be required to get his books of accounts audited. If in case he is declaring profits less the 8% of turnover (6% in case of sale is through banking channels), then we have to check two more conditions:

1. Whether in any of the preceding previous years, the person has declared profits as per sec 44AD.

AND

2. Whether the income of the person exceeds the basic exemption limit.

If both the above conditions are satisfied, then the person is required to get books of accounts audited. In case any of the condition is not satisfied or both the conditions are not satisfied, then the person would not be required to get the books of accounts audited.

(a) A person who has started a new business

It is a very interesting issue in which an assessee who has started a new business during the previous year and he is unable to decide whether to opt for sec 44AD of the Act or not. If he decides to avail the benefits of sec 44AD, then he has to declare profits at the rate of 8% or 6% of turnover or at higher rate as specified in sec 44AD. Then he shall neither be required to maintain books of account nor required to get them audited. In case, he decides to not opt for sec 44AD, the situation will be entirely different.

In this regard, it is to be noted that the assessee who has not declared profits u/s 44AD in any of the preceding previous years and he has not failed to declare profits in subsequent 5 years as per sec 44AD. The assessee who has started his business in the previous year has not satisfied the conditions of sec 44AD(4) of the Act .Hence the assessee will not be required to get his books of account audited in first year of business if his turnover is below Rs.1 crore during the previous year. However, he will be required to maintain books of accounts as per 44AA(2)(ii) if in case of individual/ HUF turnover is likely to exceed Rs.25 Lacs or his profits are likely to exceed Rs.2.5 Lacs.

Therefore, assessee who has started a new business would not be required to get books of accounts audited even if he is declaring profits below 8% or 6% because the condition that in earlier previous year he has declared income as per sec 44AD is not satisfied. The income may be below taxable limit or higher than that.

Example: Following are the 4 assesses who have started business during the previous year and they do not want to opt the provisions of sec 44AD of the Act.

Assessee |

Turnover (Rs.) |

Income/ Profits |

Maintenance of Accounts |

Audit of Books |

A |

20,00,000 |

1,50,000 |

No |

No |

B |

20,00,000 |

3,00,000 |

Yes (profits exceeds Rs. 2.5 L) |

No |

C |

50,00,000 |

3,25,000 |

Yes |

No |

D |

50,00,000 |

1,75,000 |

Yes |

No |

From combined study of sec 44AA, 44AB and 44AD, we can conclude:

Example: Mr. X started a new business in P.Y. 2020-21 and had a turnover of Rs.95 lacs and profit of Rs.5 lacs in 2020-21. The assessee wants to know whether he will he be liable to tax audit u/s 44AB.

Ans: Mr. X has started a new business in the previous year 2020-21 so he has not satisfied the conditions of sec 44AD(4) of the Act Hence he will not be required to get his books of account audited in first year of business if his turnover is below Rs.1 crore during the previous year. However, he will be required to maintain books of accounts as per 44AA(2)(ii)

Example: Mr. X is a Chartered Accountant and started a professional firm during the previous year 2020-21 and had a turnover of less than Rs.50 lacs in PY- 2020-21 and profit of less than 50%. Whether he will he be liable to tax audit u/s 44AB.

Ans: Since the assessee is engaged in profession and not business in this case, our answer will differ from above. Under the provision of sec 44ADA of the Act, there is no provision to refer the previous year and assessee has to see the provision year wise independently. The asseessee has to maintain the books independently and liable to be tax audit u/s 44AB(d).

(b) If an assessee who has never opted the provisions of 44AD

In this case if an assessee who has never opted the provisions of sec 44AD of the Act will not be required to get his books of accounts audited if his turnover is below Rs.1 crore even if he is declaring profits below 8% or 6% of turnover, because sec 44AD(4) of the Act is not applicable in his case. Two of the 3 conditions mentioned on combined analysis of sec 44AA(2), 44AB(e) and 44AD(4) are not satisfied in this case i.e. assessee has not declared income u/s 44AD in any previous year and assessee has not failed to opt sec 44AD in subsequent 5 years. It does not matter whether the income is below the basic exemption limit or higher than the basic exemption limit. This will be applicable for the person not only in the first year, rather in later years also. If in later years he has not declared income u/s 44AD even once, he would not be required to get books of accounts audited even his profits are below the rates provided in sec 44AD provided turnover is below Rs.1 crore.

A.Y. |

Turnover (Rs.) |

Income/ Profits |

Maintenance of Accounts |

Audit of Books |

2016-17 |

1,35,00,000 |

4,00,000 |

Yes |

Yes 44AB(a) |

2017-18 |

2,50,00,000 |

5,50,000 |

Yes |

Yes 44AB(a) |

2018-19 |

1,25,00,000 |

3,00,000 |

Yes |

Yes 44AB(a) |

2019-20 |

80,00,000 |

3,25,000 |

Yes 44AA(2)(i) |

No |

2020-21 |

50,00,000 |

1,75,000 |

Yes 44AA(2)(i) |

No |

2021-22 |

75,00,000 |

4,25,000 |

Yes 44AA(2)(i) |

No |

From the above table it is clear that under this situation, assessees who have never ever opted for the scheme till the AY 2016-17 can enjoy the benefits by showing lesser profits for the subsequent assessment year.

(c) A person who has opted for Sec 44AD(1) in any of the previous year and in subsequent 5 previous years, declares profits to be lower than the 8% or 6% of turnover:

In such a situation, if a person who has opted presumptive taxation in the previous year and he can opt for the same in the current year also. But in case he does not want to opt the provisions of presumptive taxation, he will be liable to maintain books of accounts and get them audited under section 44AB(e) of the Act

In previous year 2018-19, the person has opted out of sec 44AD(1). Therefore in next 5 previous years i.e. upto P.Y. 2023-24, he is compulsorily required to get books of account audited u/s 44AD(e) irrespective of profits declared. It is to be noted that in P.Y. 2020-21, the income of the assesse is below the taxable income, the person is not required to get his books of accounts audited.

Previous Year |

Turnover (in Lacss) |

Profit % |

Whether cash Receipts/Payments up to 5% of total receipts/ payments |

Whether income above basic exemption limit |

Whether audit required? |

2017-18 |

80 |

9% |

Yes |

Yes |

No |

2018-19 |

75 |

5% |

No |

Yes |

Yes [Sec 44AB(e)] |

2019-20 |

62 |

10% |

Yes |

Yes |

Yes[Sec44AB(e)] |

2020-21 |

48 |

4% |

Yes |

No |

No |

2021-22 |

99 |

7% |

No |

Yes |

Yes [Sec 44AB(e)] |

Note- The exemption from audit if cash receipts are upto 5% of total receipts and cash payments are up to 5% of total payments is not applicable if turnover is upto 1 crore. The proviso for exemption from audit is given below the clause (a) of Sec 44AB i.e. only in cases where turnover is above Rs.1 crore. The method of receipts and payments is irrelevant if the turnover is less than or equal to Rs.1 crore

(d) No audit is required if turnover is up to Rs.1 crore and taxable income is below exemption limit

From the reading of provisions of the sec 44AD(5), it is concluded that there are two conditions of sec 44AD(5) of the Act. The first is regarding applicability of provisions of sec 44AD(4) of the Act and the second is that the income of assessee is more than the basic exemption limit. These both conditions are connected with word “and”. These two conditions must be fulfilled simultaneously. If the assessee fails to fulfill any one condition or both, then the assessee is not required to maintain books of account and not to get the accounts audited.

In other words, we can say that the assessee is bound to get the books of accounts audited, if the following two conditions are satisfied:-

-

Earlier assessee has declared income u/s 44AD in any previous year and assessee do not declare income as per sec 44AD in any of next 5 A.Ys in which he first declared income as per sec 44AD.

-

The total income of the assessee exceeds the maximum amount which is not chargeable to income tax

To claim the benefit of above sec 44AD(5),firstly we have to see the meaning of total income. As per sec 2(45) of the Act, Total income means the total amount of income referred to in section 5 computed in the manner laid down in the Act. Thus total income for the purpose of Sec 44AD(5) would be determined as under :

-

i) Income from all heads of income be aggregated after adjusting for brought forward losses, unabsorbed depreciation, etc. and after excluding exempt incomes;

-

ii) From the resultant, amount eligible for deduction under Chapter VI-A will be deducted.

iii) Balance will be total income for the purposes of section 44AD(5)

If the total income is below the maximum amount not chargeable to tax in the case of assessee then the assessee will not be required to maintain books and get them audited if he declares profit from eligible business lower than that deemed under section 44AD.

Further, if any individual/HUF has incurred loss, then also there is no need to maintain books and to get them audited.

(e) No audit of a person other than resident individual/HUF/Partnership Firm

-

It is noteworthy that an assessee except resident individual/HUF/Partnership Firm eligible u/s 44AD, such as company or a LLP shall not be required to get its accounts audited u/s 44AB of the Act, even if there:

-

gross receipts during the year does not exceed Rs.1 Crore,

-

they report profit lower than the presumptive rate of 6 percent or 8 percent as the case may be, and

-

their taxable income exceeds maximum amount of taxable income not chargeable to tax.

-

(f) Assessee has not opted for presumptive taxation because of commission income

As per the provisions of sub section 6 of section 44AD, if an assessee has earned any income from specified activities such as commission, then provisions of section 44AD shall have no bearing on such assessee .In such a case, the assessee is not entitled to opt the provisions of sec 44AD.If ,in a year, the chain of sec 44AD is broken due to the receipt of commission ,that will not be considered as the assessee has gone out of the umbrella of sec 44AD.The asseessee is entitled to opt for sec 44AD in subsequent years.

It can be implied that where an assessee has turnover less that threshold specified u/s 44AB(1) and have earned any income as commission or brokerage, then he can file income with lower profits without getting its books of account audited.

Turnover of Mr. X for the F.Y. 2019-20 was Rs.74 Lacss. He has opted for Sec 44AD in that year. In the F.Y. 2020-21, his turnover was Rs.60 Lacss. Besides this turnover, his commission receipts were Rs.5,000. He could not opt for Sec 44AD as per the provisions of Sec 44AD(6). Whether he can avail the benefit of Sec 44AD from F.Y. 2021-22?

Mr. X was having commission income in the F.Y. 2020-21 and was not eligible for Sec 44AD. As per the provisions of Sec 44AD(6), a person cannot opt for Sec 44AD, if he is having commission income. He has not opted out of Sec 44AD on his own, rather he was not eligible by the operation of law. Hence he can opt for Sec 44AD in the F.Y. 2021-22.

-

When business turnover is exceeding Rs.1 crore but upto Rs.2 crore

The turnover limit for audit u/s 44AB(a) is Rs.1 crore. However, Sec 44AD allows a person to declare profits @ 8% or 6% of turnover if turnover is up to Rs.2 crores. This makes the interplay of Sec 44AB and 44AD more interesting. In such a situation, a person may come across the following situations : |

(a) New business started during the previous year

In such a situation, if a person has cash receipts and payments less than 5% then by virtue of the proviso to sec 44AB(a), he is not required for tax audit. But if his cash receipts and payments from business are more than 5% then he is liable for audit under section 44AB(a) of the Act. In both the cases, he has to maintain the books of account . It is also open to the person who has turnover upto Rs.2 crores to declare profits @8% or 6% of the turnover. In such a situation that person will not be liable for audit and maintenance of books of accounts.

Example: Mr. X has started a new business in P.Y. 2020-21 and has turnover of Rs. 1.5 crore. Whether he will be liable for audit u/s 44AB?

Ans. If the cash receipts and payments from business of Mr. X are more than 5% then he is liable for audit under section 44AB(a) of the Act. Since his turnover is upto Rs. 2 crores he has a option to declare profits @8% or 6% of the turnover. In such a situation that person will not be liable for audit and maintenance of books of accounts. If the cash receipts and payments from business of Mr. X are less than 5% then he will not be liable for audit.

(b) A person who has opted presumptive taxation during any of the previous year

In such a situation, if a person who has opted presumptive taxation in the previous year and he can opt for the same in the current year also. But in case he does not want to opt the provisions of presumptive taxation, he will be liable to maintain books of accounts and get them audited under section 44AB(e) of the Act. It does not matter whether his transactions are less than or more than 95% in any mode other than cash. In this connection, it is to be noted that the proviso to section 44 AB(a) is not applicable to section 44AB(e) of the Act.

Example: Mr. X is engaged in a business of trading of goods. During FY 2019-20 relevant to AY 2020-21, he reported Total turnover of the business as Rs.1.45 Crore, entire sales were made in cash. Mr. X computed profit from the aforesaid business to be Rs.6.80 Lakh which was his sole income during the year. During FY 2017-18 and FY 2018-19, he opted for presumptive taxation scheme u/s 44AD. Whether Mr. X is required to get his accounts audited u/s 44AB ?

Ans. Mr. X is required to get his accounts audited u/s 44AB(e) of the Act as he had claimed profit from business less than deemed income u/s 44AD i.e., actual income of Rs.6.80 Lakh is less than deemed income of Rs.11.6 Lakhs (8% of 1.45 Crore). Whereas, total income of assessee for the FY 2019-20 exceeds the maximum amount not chargeable of tax. {Section 44AD(5)}

Also, Mr. X Shall not be allowed to avail the benefit of presumptive taxation for next 5 assessment years as well i.e., AY 2021-22 to AY 2025-26 as he was eligible for opting for presumptive taxation u/s 44AD for A.Y. 2020-21 but had not opted for the same [Section 44AD(4) r.w.s. 44AB(e)].

(c) A person who has not opted presumptive taxation in any of the previous year

If a person who has not declared profits u/s 44AD in any previous year and for the current financial year he does not want to opt the provisions of the presumptive taxation then he would be liable for audit under sec 44AB(a)of the Act. If he wants to opt the provisions of presumptive taxation then he is not liable to maintain books of accounts and get them audited.

(d) A person having income below the basic exemption limit

In such a scenario, the following situations may emerge

-

If a person who has declared profits u/s 44AD in any of the preceding previous year, and he does not want to opt the provisions of presumptive taxation for the current year. His total income is below the exemption limit, even then the audit would be conducted as per the provisions of sec 44AB(a). In such a situation, he can take the benefit of proviso to section 44AB(a).

-

If a person who has failed to opt the provisions of presumptive taxation under section sec 44AD(1) and his income is above the basic exemption limit, then he will be required to get his books of accounts audited u/s sec 44AB(e) even if he declares profits above 8% or 6% of turnover.

Example: Mr. X is engaged in a business of trading of goods. During FY 2020-21 relevant to AY 2021-22, he reported Total turnover of the business Rs.1.47 Crore, entire sales were made in cash. Mr. X computed profit from the aforesaid business to be Rs.2.15 Lacs which was his sole income during the year. During FY 2018-19 and FY 2019-20, he opted for presumptive taxation scheme u/s 44AD. Whether Mr. X is required to get his accounts audited u/s 44AB for F Y 2020-21?

-

X is required to get his accounts audited u/s 44AB(a) of the Act as total income of assessee for the FY 2020-21 relevant to AY 2021-22 is less than maximum amount not chargeable to tax even if he had claimed profit from business less than deemed income u/s 44AD i.e., actual income of Rs.2.15 Lacs is less than deemed income of Rs.11.76 Lacs (8% of 1.47 Crore).

However, Mr. X shall not be allowed to avail the benefit of presumptive taxation for next 5 assessment year as well i.e., AY 2022-23 to AY 2026-27 as he was eligible for opting for presumptive taxation u/s 44AD for A.Y. 2021-22 but had not opted for the same. (Section 44AD(4) r.w.s. 44AB(e)).

This implies that if in AY 2022-23 to AY 2026-27, his total income exceeds maximum amount not chargeable to tax, he shall be mandatorily required to get his accounts audited u/s 44AB irrespective of the fact that his profit from such business exceeds deemed profit stipulated u/s 44AD(1).

(e) A Person who has received commission during the year

A restriction under section 44AD(6) of the Act has been imposed that a person receiving any commission or brokerage cannot opt for the provisions of presumptive taxation. If it is the first year of business and the person receives any commission then he cannot opt the benefits of presumptive taxation. That person will have to get his books of accounts audited under section 44AB(a) of the Act. In such a case, the assessee can avail the benefit of proviso to the section 44AB(a) of the Act.

As per the provisions of sub section 6 of section 44AD, if an assessee has earned any income from specified activities such as commission, then provisions of section 44AD shall have no bearing on such assessee .In such a case, the assessee is not entitled to opt the provisions of sec 44AD.If ,in a year, the chain of sec 44AD is broken due to the receipt of commission ,that will not be considered as the assessee has gone out of the umbrella of sec 44AD.The asseessee is entitled to opt for sec 44AD in subsequent years.

Example: Mr. X is engaged in a trading business. In P.Y. 2020-21 his turnover is Rs.1.5 crores (all by digital mode) Also he has received Rs.5,000 as commission income. Profit shown as per books is Rs.2,40,000. In P.Y. 2018-19 and P.Y. 2019-20 he has opted for presumptive taxation. Whether he is liable to get his accounts audited u/s 44AB?

Answer: MR. X is not eligible to opt the provisions of presumptive taxation by virtue of the provisions of section 44AD (6) of the Act. In this case the provisions of Section 44AB (a) will be applicable and not Section 44AD (e). However by virtue of proviso to Section 44AB (a), he is not liable to get his books of accounts audited.

(f) Professional firms falling under this category whether they are 95 or not have audit and accounts because the proviso is applicable to sec 44ab(a) of the Act.

This can be understood with the help of an example. Mr. X has started business on 01.04.2019.

Previous Year |

Turnover (in Lacss) |

Profit % |

Whether cash Receipts/Payments up to 5% of total receipts/ payments |

Whether income above basic exemption limit |

Whether audit required? |

2019-20 |

150 |

5% |

Yes |

Yes |

No [Proviso to sec 44AB] |

2020-21 |

140 |

5% |

No |

No |

Yes [44AB(a)] |

2021-22 |

120 |

10% |

Yes |

Yes |

No |

2022-23 |

175 |

4% |

No |

No |

Yes [44AB(a)] |

2023-24 |

175 |

4% |

Yes |

yes |

Yes [44AB(e)] |

(c) When business turnover exceeding Rs.2 crore but upto Rs.10 crore

As per the proviso to section 44AB (a),in cases where the aggregate cash receipts and aggregate cash payments made during the year from business does not exceed 5% of total receipt and total payment respectively the assessee is not liable to get his books of accounts audited under section 44AB(a) if his turnover does not exceed Rs.10 crores. However if the less than 95% of the business transactions is done through banking channels, the assessee is liable to get his books of accounts audited. This provision is only applicable if the assessee is engaged in a business and not in a profession. A person engaged in a profession is liable to get his books of accounts audited under section 44AB(b) if his turnover exceeds Rs.50 Lakhs.

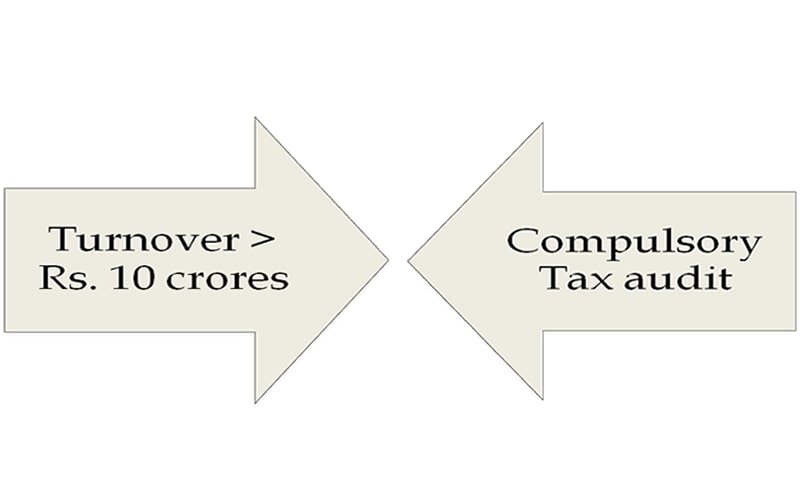

(D) When business turnover exceeding Rs.10 crore

A person engaged in business whose turnover exceeds Rs.10 crores is liable to get his books of accounts audited under section 44AB even if more than 95% of the business transactions is done through banking channels. It is to be noted that the proviso to section 44AB(a) is only applicable to a person engaged in a business. A person engaged in a profession is liable to get his books of accounts audited under section 44AB(b) if his turnover exceeds Rs.50 Lakhs.

Comprehensive Table

Covering all situations in the interplay of Sec 44AA, 44AB and 44AD:

Case |

Turnover |

Whether total income below exemption limit |

Whether cash receipts/ payments upto 5% of total receipts/ payments |

Whether opted for Sec 44AD in any of the preceding year |

Rate of profits declared as %age of turnover |

Whether required to maintain books u/s 44AA(2) |

Whether required to get books of accounts audited |

A(a) |

Up to Rs.1 crore |

Yes |

Irrelevant |

No |

8% |

Note 1 |

No |

(b) |

Up to Rs.1 crore |

No |

Irrelevant |

Yes |

4% |

Yes |

Yes |

(c) |

Up to Rs.1 crore |

Yes |

Irrelevant |

No |

4% |

Note 1 |

No |

(d) |

Up to Rs.1 crore |

No |

Irrelevant |

Yes, But opted out from Sec 44AD in any of the preceding 5 years |

10% |

Yes |

Yes u/s 44AB(e) |

(e) |

Up to Rs.1 crore |

Yes |

Irrelevant |

Yes |

4% |

Note 1 |

No |

B(a) |

Rs.1 crore- Rs.2 crores |

No |

Yes |

No |

5% |

Yes |

No [Proviso to Sec 44AB(a)] |

(b) |

Rs.1 crore- Rs.2 crores |

Yes |

No |

Yes |

5% |

Yes |

Yes u/s 44AB(a) |

(c) |

Rs.1 crore- Rs.2 crores |

Yes/No |

No |

Yes |

9% |

Yes |

No |

(d) |

Rs.1 crore- Rs.2 crores |

No |

No |

Yes, But opted out from Sec 44AD in any of the preceding 5 years |

10% |

Yes |

Yes u/s 44AB(e) |

(e) |

Rs.1 crore- Rs.2 crores |

Yes |

No |

Irrelevant |

5% |

Yes |

Yes u/s 44AB(a) |

C(a) |

Rs.2 crores-Rs.10 crores |

Irrelevant |

Yes |

Irrelevant |

Irrelevant |

Yes |

No [Proviso to Sec 44AB(a)] |

(b) |

Rs.2 crores-Rs.10 crores |

Irrelevant |

No |

Irrelevant |

Irrelevant |

Yes |

Yes, Sec 44AB(a) |

D |

Above Rs.10 crores |

Irrelevant |

Irrelevant |

Irrelevant |

Irrelevant |

Yes |

Yes |

{kind=link}

{kind=link}