![]()

BACK TO BASICS: DEBITS AND CREDITS

"Going back to the basics strengthens your foundation".

All the business transactions are either tracked as debits or credits.

Three golden rules of accounting:

Personal Accounts: Debit the receiver; credit the giver

Real Accounts: Debit what comes in, credit what goes out

Nominal Accounts: Debit all expenses and losses, credit all incomes

and revenues

Journal entry is recording of a transaction. A transaction is recorded as debits

and credits. Each debit to an account must be accompanied by a credit to

another account. Luca Pacioli the "Father of Accounting" said that you should

not go to sleep until your debits equalled your credits.

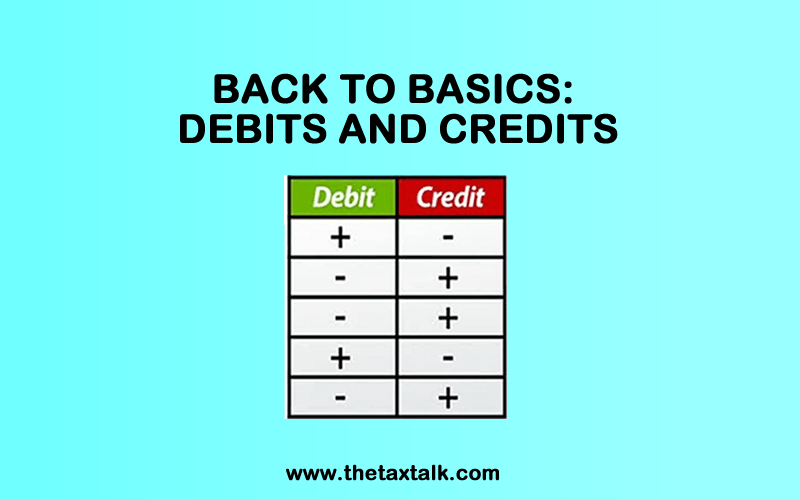

Assets = Liabilities + Owners equity. An increase in the value of assets is a

debit to the account, and a decrease is a credit. An increase in liabilities or

owners equity is a credit to the account, and a decrease is a debit.

{kind=link}

{kind=link}