![]()

An overview of the provision related to set off and carry forward of Loss under the Income Tax Act – 1961 : CA Sahil Dhingra

INTRODUCTION:

Set off means adjustment of losses against the

profits from another source/other head of income in the same assessment year. If such losses can-not be set-off in the same year due to Inadequacy of eligible profits, then such losses are carried forward to the next assessment years for adjustment against the eligible profits of that year.

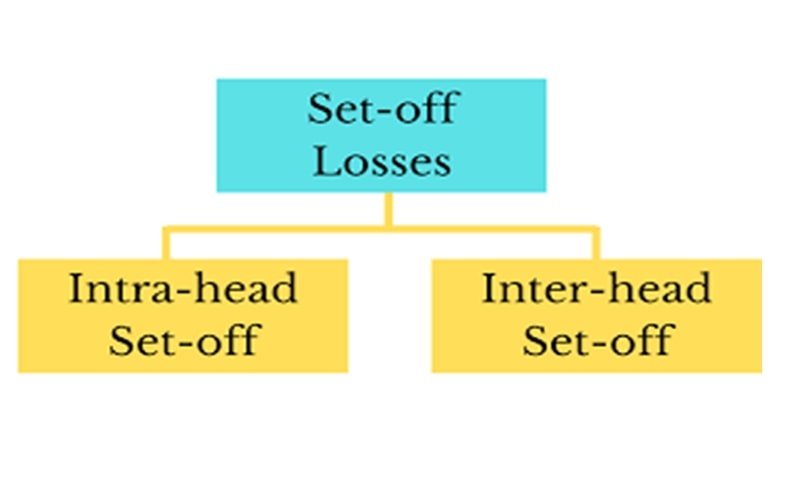

INTRA HEAD SET OFF:

INTRA HEAD SET OFF:

- Loss incurred in respect of one source shall be set-off against income from any other source under the same head of income

- The Income under each head is to be computed by grouping together the net result of the activities of all the sources covered by that head.

Some Exceptions for Intra Head Set-off are as follows:

- Long Term Capital Loss {Section 70(3)}

Short-term capital loss is allowed to be set-off against both short-term capital gain and long term capital gain. However, long-term capital loss can be set off against long-term capital gain and not short-term capital.

- Speculation loss {Section 73(1)}

A loss in speculation business can be set-off only against the profits of any other speculation business and not against any other business or professional income.

- Loss from the activity of owning and maintaining race horses {Section 74A(3)}

Such loss can be set-off against income from the activity of owning and maintain horse races.

- Losses from specified business {Section 73A(1)}

A loss in any specified business referred in section 35AD can be set-off only against any other specified business.

However, losses from other business can be set off against profits from specified business.

Note: Loss from an exempt source cannot be set-off against profits from a taxable source of income. {Example: Share of loss from partnership firm cannot be set-off against business income, since share of income of the firm is exempt under section 10(2A)}.

INTER HEAD SET OFF:

- Loss under any head other than capital gains:

Where the net result of the computation under any head of income other than capital gains is a loss, the assesse can set-off such loss against his income assessable for that assessment year under any head, including capital gains.

- Loss under the head Profit and gains from business or profession:

Where the net result of the computation under the head PGBP is a loss, such loss cannot be set off against income under the head salaries.

- Loss under the head Capital Gains:

Where the net result of computation under the head capital gains is a loss, such capital loss cannot be set-off against income under any other head.

- Loss under the head Income from house property:

Where the net result under the head Income from House Property is a loss then maximum loss of Rs. 2 Lakhs can be set-off against income from any other head.

- Speculation loss, loss from the activity of maintaining race horses and losses from specified business referred to in section 35AD:

It cannot be set-off against income any other head

SUMMARY OF INTRA HEAD & INTER HEAD SET OFF LOSS

| Category | Salary Income | House Property Income | Non- Speculative Business Income | Speculative Business Income | LTCG | STCG | Horse Race Income | Other Sources Income |

| House Property Loss (UptoRs 2 Lakhs) | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Speculative Business loss | No | No | No | Yes | No | No | No | No |

| Non- Speculative business loss | No | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| LTCL | No | No | No | No | Yes | No | No | No |

| STCL | No | No | No | No | Yes | Yes | No | No |

| Horce Race Losses | No | No | No | No | No | No | Yes | No |

| Other Source Losses | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

CARRY FORWARD OF LOSSES

- Carry forward of Loss under the Head House Property

{ Section 71B}:

The loss under this head is allowed to be carried forward upto 8 Assessment years immediately succeeding the assessment years in which the loss was first computed.

It can be set off only against the income from the same head in the forthcoming assessment years.

- Carry forward of Loss under the head PGBP {Section 72}:

Due to the absence or inadequacy of income under any other head in the same year the loss carried forward can be set-off against the business profits of subsequent years.

However, loss carried forward cannot, under any circumstances, be set-off against the income from any head other than PGBP.

A business loss can be carried forward for a maximum period of 8 assessment years immediately succeeding the assessment year in which the loss was incurred.

- Carry Forward of Loss in Speculation Business {Section 73}:

Speculation Business is deemed to be a distinct business and separate from any other business carried on by the assesse, the losses incurred in speculation can be neither set off in the same year against any other non- speculative income nor be carried forward and set-off against other income in the subsequent years.

Therefore, the losses sustained by the assesse in a speculation business cannot be set-off in the same year against any other speculation profit, they can be carried forward to subsequent years and set-off only against income from any speculation business carried on by the assesse.

The loss in speculation business can be carried forward only for a maximum period of 4 years from the end of the relevant assessment year in respect of which loss was computed.

Loss from the activity of trading in derivatives is not treated as speculation loss.

- Carry Forward of loss by Specified Business {Section 73A}:

Any loss computed in respect of the specified business referred to in section 35AD shall be set-off only against profits and gains of any other specified business. The unabsorbed loss, if any will be carried forward for set-off against profits and gains of any specified business in the following assessment year and so on.

Specified Business Loss can be Carried Forward for indefinite period.

- Carry Forward of Loss under the Head Capital gains

{Section 74}

Any unabsorbed loss shall be carried forward to the following assessment year uptomaximum of 8 Assessment years immediately succeeding the assessment year for which the loss was first computed.

- Carry Forward of Loss from the activity of Owning and Maintaining Horse Races {Section 74A(3)}:

Such loss can be Carried Forward for a maximum period of 4 years immediately succeeding the assessment year for which the loss was first computed, for being set-off against the income from the activity of owning and maintaining race horses.

ORDER OF SET-OFF LOSSES:

- Current year Depreciation. {Section 32(1)}

- Current year capital expenditure on scientific research and current year expenditure on family planning, to the extent allowed.

- Brought forward loss from business/profession.

{Section 72(1)}

- Unabsorbed depreciation. {Section 32(2)}

- Unabsorbed capital expenditure on scientific research. {Section 35(4)}

- Unabsorbed expenditure on family planning.

{Section 36(1)(ix)}

| S. No. | Type of Loss | Time Limit for Carry Forward |

| 1. | House Property | 8 Years |

| 2. | Speculation Business | 4 Years |

| 3. | Other Business Losses | 8 Years |

| 4. | Short Term Capital Loss | 8 Years |

| 5. | Long Term Capital Loss | 8 Years |

| 6. | Specified Business | No Limit |

| 7. | Owning & Maintaining Horse Races | 4 Years |

| 8. | Unabsorbed Depreciation | No Limit |

Income Tax Act on Your Mobile Now Android Application For Income Tax Act – 1961 with Cost Inflation Index and other tools on Mobile now at following link:

Whatsapp Group at

{kind=link}

{kind=link}